Health premiums vs income/payroll taxes

What's the real tax on US workers?

Executive summary

For the typical American worker, healthcare-related premiums/taxes aren’t just “big.” They’re bigger than all non-healthcare-related income/payroll taxes combined. Healthcare is THE thing impacting take-home pay.

If we call employer-sponsored health insurance what it is - a tax - then about 70% of taxes taken from the paychecks of a typical American worker with family coverage go to healthcare. If the worker has individual coverage, that number is about 51%.

In hard dollars, the healthcare industry takes about $26,000 from the total compensation of a worker with family coverage whose salary is $50,000 (whose total compensation is actually about $70,000).

The structure and branding of healthcare financing (having the employer pay the bulk of it, and calling it a "premium" instead of a "tax”) leads the typical American to grossly underestimate 1) their healthcare costs and 2) their total taxes.

Because the US healthcare system is structured to overpay by 2x, this typical worker is overtaxed by about $13,000.

Introduction and background

A couple days ago, KFF published its annual Employer Health Benefits Survey. The report is always a treasure trove of information on employee health benefits.

While I love the report, I've always felt that it's missing one important piece of context: how do health insurance premiums compare to the income/payroll taxes paid by typical workers?

After all, health insurance premiums are money taken out of workers' paychecks, so they're essentially just another tax, albeit with better branding. Of course, participating in employer-sponsored insurance and paying the associated premiums isn't technically mandatory, and the term "tax" implies a mandatory nature. But practically speaking, due to the tax incentives in place, participating in employer-sponsored insurance might as well be mandatory, at least for one earner per household. Ergo, we might as well call premiums “taxes.”

With that “premiums are taxes by another name” idea in mind, I've used talent.com's tax calculator in conjunction with KFF survey data to whip together a brief premiums-vs-income-and-payroll-taxes comparison.

Also, I took the analysis one step further. Some portion of income/payroll taxes go towards government health programs, so premiums aren't the only way the healthcare industry is impacting workers' take-home pay. If we combine health insurance premiums with healthcare-related income/payroll taxes (i.e., the share of income/payroll taxes that go towards governmental healthcare expenditures), how much of the money taken out of employees' paychecks goes to the healthcare industry? That is, what's the total financial impact of healthcare expenses on workers' take-home pay?

Disclaimer: this is a quick, crude, back-of-the-envelope analysis. I've glossed over a lot of details for the sake of brevity. I've used terms like "total compensation" loosely. I've used 2021 data for some figures, and used 2019 data for others. I haven't accounted for family-related tax deductions when comparing family coverage to individual coverage. I have no particular expertise in taxation issues. I'd welcome refinement of this analysis by someone with more taxation experience (and more time!) than me. If time permits, I may refine it myself, too.

Breaking down the numbers

NOTE: If you don't want to dig into the details, and you prefer to skip straight to the results, you might want to move on to the next section ("Observations"). If you want to see how the sausage is made, here we go...

For a "typical" worker, I've chosen a worker making $50,000 a year in Iowa. I chose Iowa because at a quick glance its state income tax burden seemed close to the US median at this income level. (Note: "at this income level" is important since most state income tax schedules are progressive.) I set the salary at $50,000 as a rounded approximation of median pay for a full-time worker.

I've also chosen to call this typical worker "Juju" because it's a great name, and more people should be named Juju. (My first thought was to call our typical worker “Tippy.” You’re welcome.)

According to talent.com's tax calculator, Juju (our typical worker) will face a total tax burden of $14,498 in taxes. Juju will see $10,253 of these taxes; $4,245 will be taken from his paychecks without him seeing it. (This is the "taxberg" graphic on talent.com's tool.)

Per Kaiser's survey, if Juju chooses family coverage, he'll pay $22,221 in premiums. Juju will see $5,969 being deducted from his paychecks, but he won't see the additional $16,252 being paid by his employer.

You'll note that with respect to taxes, Juju sees 71% of the taxes taken from his paycheck ($10,253 / $14,498), but with respect to healthcare premiums, he only sees 27% ($5,969 / $22,221). Healthcare is sneaky like that.

So, Juju is paying $14,498 in taxes and $22,221 in premiums for a total of $36,719 in "money taken from his paychecks." (Again, I think healthcare premiums should be called "taxes" so I don't have to awkwardly type out "money taken from his paychecks," but I somehow think the industry doesn't want the branding of "taxes.") But anyways, $36,719 is a ton of money!

How is it possible to take $36,719 out of Juju's paychecks when Juju only makes $50,000? It's because of the $4,245 in "hidden" taxes and $16,252 in "hidden" premiums that are paid directly by his employer. Juju's employer is actually setting aside $70,497 ($50,000 + $4,245 + $16,252) in total compensation for Juju.

Hopefully, you immediately noticed that Juju is paying more in healthcare premiums ($22,221) than he's paying in income/payroll taxes ($14,498). 61% of the total money taken from Juju's paychecks goes to healthcare premiums ($22,221 / $36,719)!

But the $22,221 in premiums isn't all that Juju contributes towards healthcare from his paychecks. Obviously, some of the $14,498 he pays in income/payroll taxes goes to healthcare, too; funding for Medicare, Medicaid, Veteran's Administration expenses, NIH expense, etc has to come from somewhere. But how much? $1,000? $10,000? Here's where the analysis gets tricky.

On the payroll tax side, things are simple: Social Security payroll taxes are earmarked for Social Security (i.e., not healthcare); Medicare payroll taxes are earmarked for Medicare (i.e., healthcare). However, on the income tax side, reconciling taxes with healthcare spending is challenging. There are the issues of non-income/payroll federal taxes (corporate taxes, excise taxes, etc), non-income/payroll state/local taxes (property taxes, sales taxes, etc), non-tax funding (Medicare premiums), federal-to-state transfers, debt financing, and so on, and so on. There's a path to calculating a precise, defensible number here, but it's a long one.

In lieu of undertaking the lengthy reconciliation effort to determine exactly how much of Juju's $14,498 in federal/state income taxes should be attributed to healthcare expenditures vs non-healthcare expenditures, I'm going to take a crude shortcut: I'm going look at the percentage of federal government expenditures that are healthcare-related and apply that same percentage to Juju's total income/payroll taxes.

This is obviously a crude, imprecise approach, but it's Saturday, and I'm not getting paid for this.

In FY2019, the federal government spent $1.2T on healthcare out of total outlays of $4.4T. $1.2T / $4.4T = 27%. Since this is such a crude technique, I'm going to round to 25%.

If 25% of Juju's $14,498 in income/payroll taxes goes towards healthcare-related government spending, then $3,625 goes to healthcare-related government spending, and $10,873 goes to non-healthcare-related government spending.

Now let's revisit our earlier numbers. Earlier, we saw that 61% of the total money taken out of Juju's paychecks went to premiums. If we add Juju's $3,625 healthcare-related income/payroll taxes to the $22,221 in healthcare premiums, we see that he contributes a total of $25,846 to the healthcare industry from his paychecks. That means healthcare expenses account for 70% of the "taxes" taken out of his paycheck ($25,846 / $36,719)!

While Juju sees his total tax burden as 21% ($10,253 / $50,000), if we consider premiums as taxes, his total tax burden is actually 52% ($36,719 / $70,497). Juju's healthcare "taxes" ($25,846) are 37% of his total compensation ($70,497).

The biggest issue with this analysis so far is that it's solely based on family coverage rather than individual coverage. KFF's survey indicates that the average premium for individual coverage is $7,739. $1,299 of that is seen (i.e., paid by the employee) while $6,440 is unseen (i.e., paid by the employer).

Here's how the various figures compare for individual coverage vs family coverage (vs no coverage):

_____________________________________Family______Individual______No coverage

Stated salary: _________________________$50,000_____$50,000_________$50,000

Total compensation: ___________________$70,497_____$60,685_________$54,245

Total health premiums: ________________$22,221_____$7,739__________$0

Employee share of health premiums: ____$5,969______$1,299__________$0

Employer share of health premiums:_____$16,253_____$6,440__________$0

Total "taxes" (incl. health premiums)_____$36,719_____$22,237_________$14,498

Total "taxes" as a % of stated salary:______73%________44%____________29%

Total "taxes" as a % of total comp:________52%________37%____________27%

Healthcare "taxes": ____________________$25,846_____$11,364_________$3,625

Healthcare "taxes" as a % of stated salary:_52%________23%____________7%

Healthcare "taxes" as a % of total comp:___37%________19%____________7%

Healthcare "taxes" as a % of total “taxes”:__70%________51%___________25%

[My apologies for the horrible formatting.]

A useful next step in this analysis would be to look at the breakdown (by headcount) of workers with family/individual/no coverage. Section 3 of the KFF survey discusses coverage rates (155M nonelderly coverered lives, 62% of workers in firms offering health benefits are covered by their own firm), but I don't see this particular breakdown.

Also, I should state the obvious: I'm not incorporating out-of-pocket costs (deductibles, copay/coinsurance, cash-pay, etc) into any of this analysis. These costs get most of the attention in the press (and are the most visible to the individual consumer), but they are far smaller than paycheck-based cash flows.

I should also note that this analysis relates specifically to taxes taken from workers' paychecks - i.e., income taxes and payroll taxes. I'm not addressing property taxes, sales taxes, and other taxes. This is an analysis on take-home pay.

Observations

With that scintillating, page-turning description of the analytical process out of the way, we can now discuss some observations/takeaways.

Observation 1: For the typical American worker, healthcare-related premiums/taxes aren’t just “big.” They’re bigger than all non-healthcare-related income/payroll taxes combined. Healthcare is THE thing impacting take-home pay.

If we call employer-sponsored health insurance what it is - a tax - then about 70% of taxes taken from the paychecks of a typical American worker with family coverage go to healthcare. If the worker has individual coverage, that number is about 51%.

In hard dollars, the healthcare industry takes about $26,000 from the total compensation of a worker with family coverage whose salary is $50,000 (whose total compensation is actually about $70,000).

You can't be concerned about high taxes and not be concerned about healthcare costs. Healthcare costs and high taxes are one and the same.

Of course, these numbers all relate to a worker making $50,000. It may shock you to hear this, but some people make more than $50,000, and some people make less than $50,000. What is true for the worker making $50,000 is not true for the worker making $150,000. As income increases, the non-healthcare-related share of taxes increases.

Observation 2: The structure and branding of healthcare financing (having the employer pay the bulk of it, and calling it a "premium" instead of a "tax”) leads the typical American to grossly underestimate their healthcare costs.

The typical American might think that healthcare is taking $5,969 a year from their paychecks, but it's actually taking $25,846. Real healthcare costs are 433% of perceived healthcare costs!

If you ask Americans whether their healthcare is expensive, they'll probably say yes. But they won't really understand HOW expensive it is.

Americans get their sense of how expensive healthcare is from the 11% in out-of-pocket costs they pay, but the other 89% of healthcare expense (the majority of which is financed through the healthcare "taxes" discussed above) is where the real financial damage is.

Observation 3: The structure and branding of healthcare financing (having the employer pay the bulk of it, and calling it a "premium" instead of a "tax”) leads the typical American to grossly underestimate their overall taxes.

Since premiums aren't called taxes, and since the employer share of premiums are hidden from view, the real tax burden on the typical American is grossly understated. If premiums aren't considered taxes, then taxes are 21% of total compensation for a typical worker with family coverage. If they are, then taxes are 52% of total compensation. Real taxes are 248% of perceived taxes!

I am by no means the first person to observe that premiums are just taxes by another name and that we therefore underestimate the tax burden on the middle class. Matt Bruenig addressed the topic in a NYT op-ed. "Premiums are just taxes by another name" is the central point of Ted Boettner's op-ed here. UC Berkeley economists Emmanuel Saez and Gabriel Zucman address the topic as well. Regardless, I think the point merits a lot more attention.

Observation 4: Since the impact of healthcare costs on the typical American's take-home pay is drastically underestimated, the impact of healthcare reform on Americans' take-home pay is drastically underestimated.

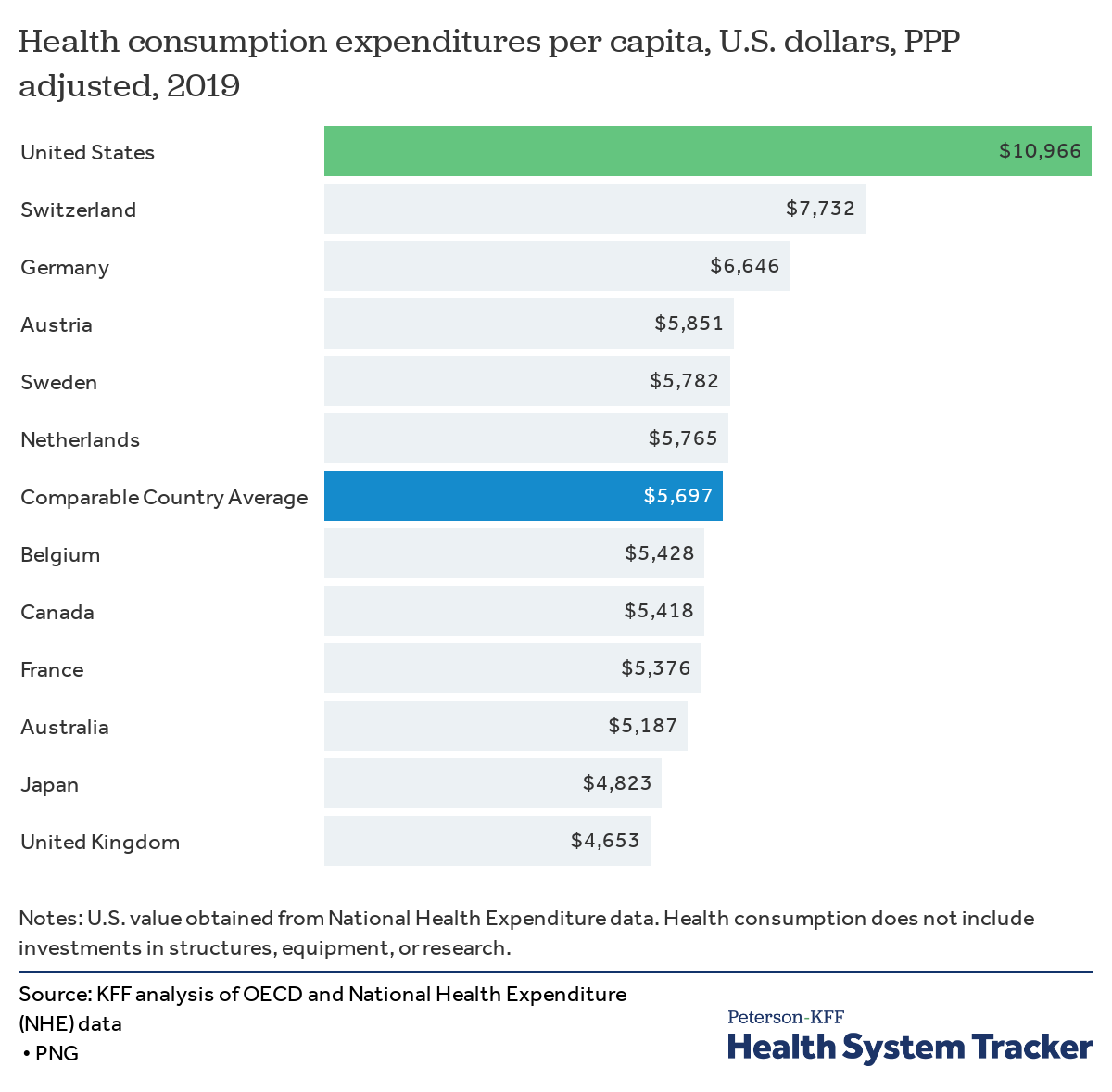

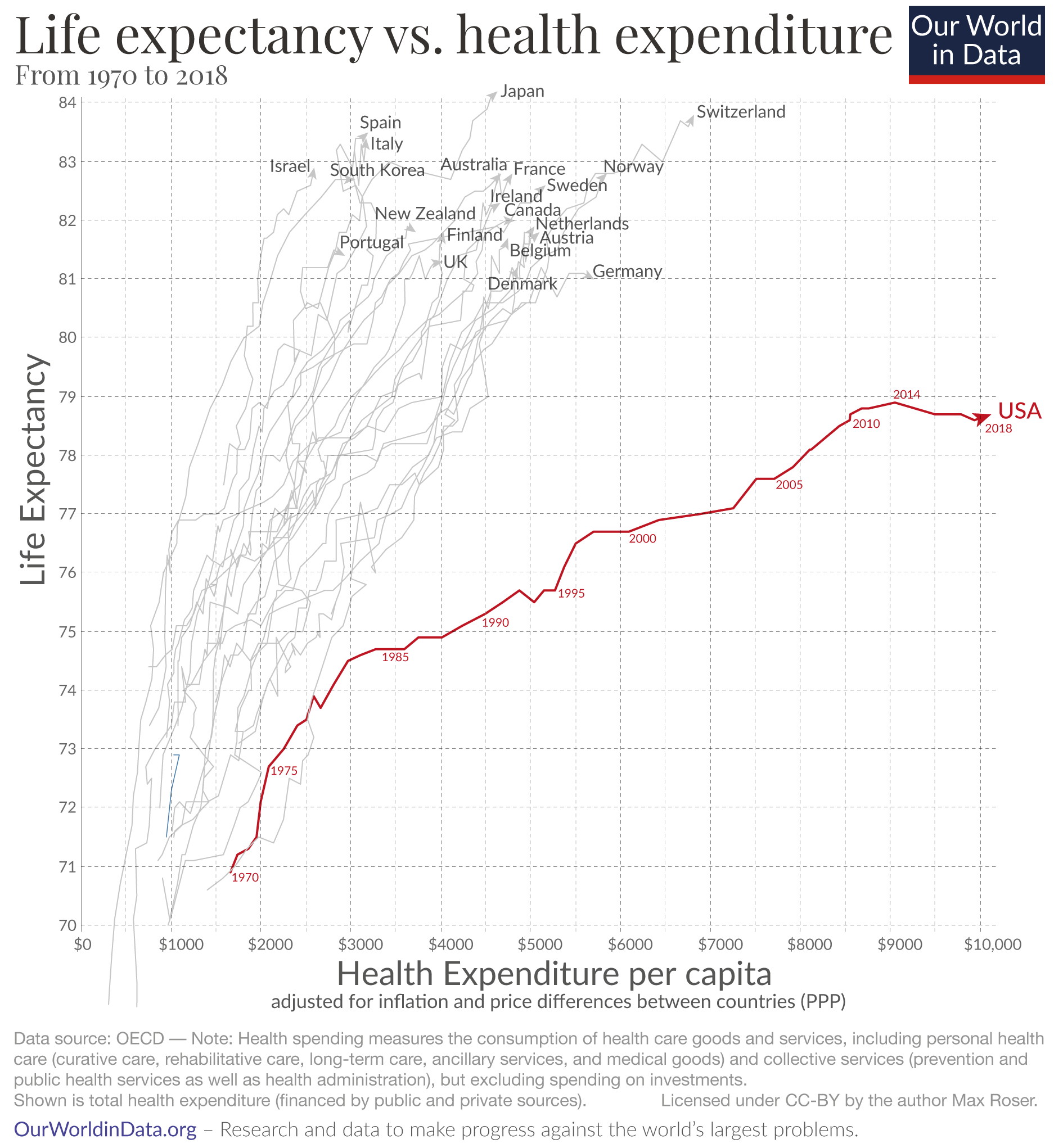

Roughly speaking, the US spends twice as much as other countries to get the same healthcare and worse outcomes. In a regular healthcare system, instead of being taxed $25,846 for healthcare, the typical American would only be taxed half of that ($12,923). In other words, the typical American is overtaxed by $12,923 (out of a salary of $50,000) to finance the excess incomes of the healthcare industry.

{kind=link}

{kind=link}

Let's say that again: The typical American with family coverage is paying $12,923 too much in healthcare taxes to finance the excess incomes of the healthcare industry. (And that doesn't even count out-of-pocket spend.)

There's a lot of literature on the relationship between premiums and wages (this article provides a summary). It's hard to say exactly how a reduction in healthcare costs would accrue to employees v employers. However, if healthcare reform were ever finally achieved, I think it’s reasonable to suspect that it would be the greatest financial boon the American middle class experiences in their lifetime.

Great article! If we were able to step back and view this issue more objectively as you've described - we would realize how much we're being deceived by simple nomenclature - premium vs. tax. Thank you for putting this together as it's quite compelling!